Managing fluctuating household expenses often feels overwhelming. While traditional banking apps track historical data, they rarely prevent overspending in real-time. A Weekly Planners printable calendar bridges this gap; it grants immediate cognitive clarity over your cash flow, provided you commit to a brief Sunday review. By tangibly mapping out concrete targets-such as grocery budgets and subscription renewals-you regain control. Below, we analyze the best layouts to streamline your financial routine.

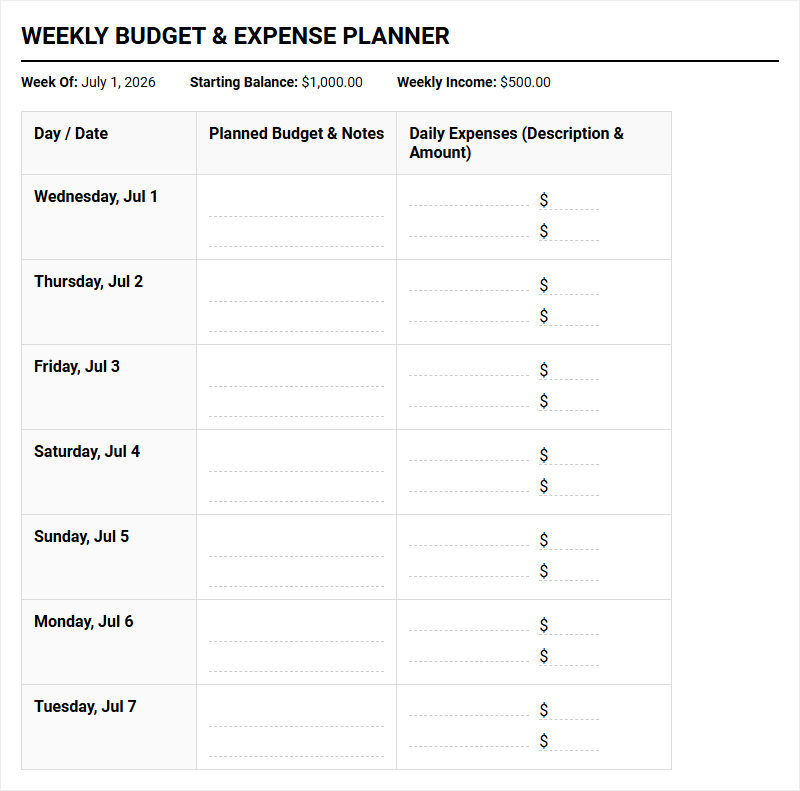

Create Your Budget and Expense Weekly Planner

| Day / Date | Planned Budget & Notes | Daily Expenses (Description & Amount) |

|---|

Done customizing?

Budget and Expense Weekly Planner - Good to Know

Zero-based budgeting

The zero-based budgeting method requires you to allocate every single dollar of your monthly income to a specific expense, savings goal, or debt repayment until your remaining balance equals exactly zero. This proactive financial strategy ensures that no money is mindlessly wasted or unaccounted for at the end of the month.

By assigning a job to every dollar, you gain complete control over your cash flow. This approach is highly effective for individuals who struggle with impulsive spending or feel unsure where their hard-earned money goes each month.

- Income: Calculate your total net monthly earnings.

- Allocation: Categorize and assign funds to rent, groceries, savings, and investments.

- Adjustment: Track transactions daily to stay aligned with your zero-sum target.

Adopting this framework fosters a deep awareness of your spending patterns, allowing you to prioritize long-term wealth building over temporary desires.

Cash stuffing

Also known as the envelope system, cash stuffing is a tactile budgeting technique that involves withdrawing physical cash and dividing it into labeled envelopes for different spending categories. When an envelope is empty, you cannot spend any more money on that category until the next budgeting cycle begins.

This method leverages psychological barriers to curb overspending. Physical cash is harder to part with than a digital card swipe, making you highly conscious of every transaction you make.

"By physically separating your money, you eliminate the temptation of digital overdrafts and impulse online purchases."

Popular categories for cash stuffing include groceries, dining out, entertainment, and personal care. It is an excellent starting point for beginners who need to break the cycle of credit card dependence and establish disciplined, visual boundaries around their disposable income.

Weekly expense tracker

A weekly expense tracker breaks down the intimidating task of monthly financial planning into manageable, seven-day increments. Instead of waiting until the end of the month to evaluate your bank account, you review your transactions weekly to make real-time adjustments before minor slip-ups escalate into major financial setbacks.

Micro-tracking your spending helps identify subtle, daily leaks in your budget, such as daily subscription services or frequent convenience store stops.

- Collect all digital receipts and bank statements every Sunday.

- Categorize expenses into fixed needs and variable wants.

- Compare the weekly total against your monthly target limits.

This habit builds consistency and reduces the anxiety often associated with personal finance management. Keeping a close eye on your weekly outlays ensures that you remain continuously aligned with your broader, long-term financial objectives.

Sinking funds

A sinking fund is a strategic savings category set aside for anticipated, non-recurring expenses that occur throughout the year. Unlike a general emergency fund, which is reserved for unexpected crises, sinking funds are created for known future events with predictable costs.

By saving a small amount regularly, you avoid the financial shock of large, sudden bills. This proactive approach keeps your monthly budget stable and prevents you from relying on high-interest credit cards when these events arise.

- Holiday shopping: Save monthly to cover year-end gifts stress-free.

- Vehicle maintenance: Prepare for annual registration, oil changes, and new tires.

- Travel plans: Accumulate funds gradually for your dream vacation.

Implementing sinking funds transforms large, intimidating expenses into manageable monthly goals, protecting your wealth and providing immense peace of mind.

Kakeibo method

Originating in Japan, the Kakeibo method is a traditional, mindful journaling approach to managing personal finances. Translated as "household account book," this practice emphasizes the philosophy of intentional spending by asking you to answer four key questions before making any purchase.

By manually writing down your income and expenses in a dedicated journal, you cultivate a deeper emotional connection to your money and learn to distinguish between true needs and passing desires.

The core Kakeibo reflection questions focus on:

- How much money do you have available?

- How much would you like to save?

- How much are you actually spending?

- How can you improve your overall habits?

This thoughtful, slow-paced financial practice encourages minimalism, reduces consumption, and helps you find satisfaction in saving rather than spending.

No-spend challenge

A no-spend challenge is a powerful financial reset where you commit to spending money only on absolute essentials for a designated period, such as a weekend, a week, or a full month. During this time, all discretionary spending is strictly paused.

This exercise forces you to find creative, free alternatives for entertainment and meals, highlighting how often you spend money out of habit or boredom. The accumulated savings from a successful challenge can be used to pay off debt or boost your savings rate rapidly.

Allowed expenses typically include rent, utilities, basic groceries, and medicine, while prohibited items include dining out, clothing shopping, and impulse purchases. Participating in these challenges rewires your relationship with consumerism, helping you realize how little you actually need to live a fulfilling and joyful life.

Debt snowball tracker

The debt snowball tracker is an organized system based on the famous debt reduction strategy popularized by financial experts. Using this method, you list all of your outstanding debts from the smallest balance to the largest, regardless of the interest rates associated with them.

You pay the minimum amount due on all accounts except the smallest one, toward which you throw any extra funds you can find. Once the smallest debt is completely paid off, you roll its payment into the next smallest balance, creating a powerful compounding effect.

| Creditor | Balance | Minimum Payment |

|---|---|---|

| Credit Card A | $500 | $25 |

| Personal Loan | $2,500 | $80 |

This strategy relies heavily on behavioral psychology. Seeing accounts close quickly builds incredible momentum and motivation, keeping you focused on the journey toward total financial freedom.

50/30/20 rule planner

The 50/30/20 rule planner is a straightforward, highly effective framework designed to simplify budgeting by dividing your after-tax income into three distinct, easy-to-manage categories. This balanced structure ensures you cover your current obligations while planning for the future.

By allocating fixed percentages, you remove the guesswork from financial planning and maintain a balanced lifestyle without feeling excessively restricted.

- 50% Needs: Essential living costs like rent, groceries, insurance, and utilities.

- 30% Wants: Discretionary spending including dining out, hobbies, and entertainment.

- 20% Savings: Future wealth building, emergency funds, and extra debt payments.

Using this ratio helps you maintain a healthy equilibrium between enjoying your present life and building robust security for your financial future.

Bi-weekly budget template

A bi-weekly budget template aligns your financial planning directly with your pay cycle if you receive compensation every two weeks. This approach helps prevent the common cash flow gaps that occur when trying to manage monthly bills with mid-month paychecks.

By dividing your monthly expenses into two halves, you can allocate portions of each paycheck to specific bills, ensuring that your obligations are consistently met without stress.

This system is particularly advantageous during months with three paychecks. You can treat these "extra" paychecks as bonus savings opportunities, directing the surplus toward your high-interest debt or investment goals. Customizing your budget to match your exact earning schedule removes confusion and helps you build a steady, predictable financial routine.

Financial self-care

Financial self-care is the practice of treating your money management as an essential component of your mental, emotional, and physical well-being. Rather than viewing budgeting as a chore or punishment, you approach your finances with kindness, intentionality, and respect.

This mindset shift involves setting regular appointments to review your accounts, forgiving yourself for past monetary mistakes, and establishing healthy boundaries around your spending and lending habits.

"Taking care of your money is taking care of your future self."

By organizing your finances, reducing debt, and investing in your growth, you actively lower your daily stress levels and open doors to new opportunities. Prioritizing your financial wellness empowers you to build a secure life that aligns perfectly with your deepest personal values.

Leave a comment