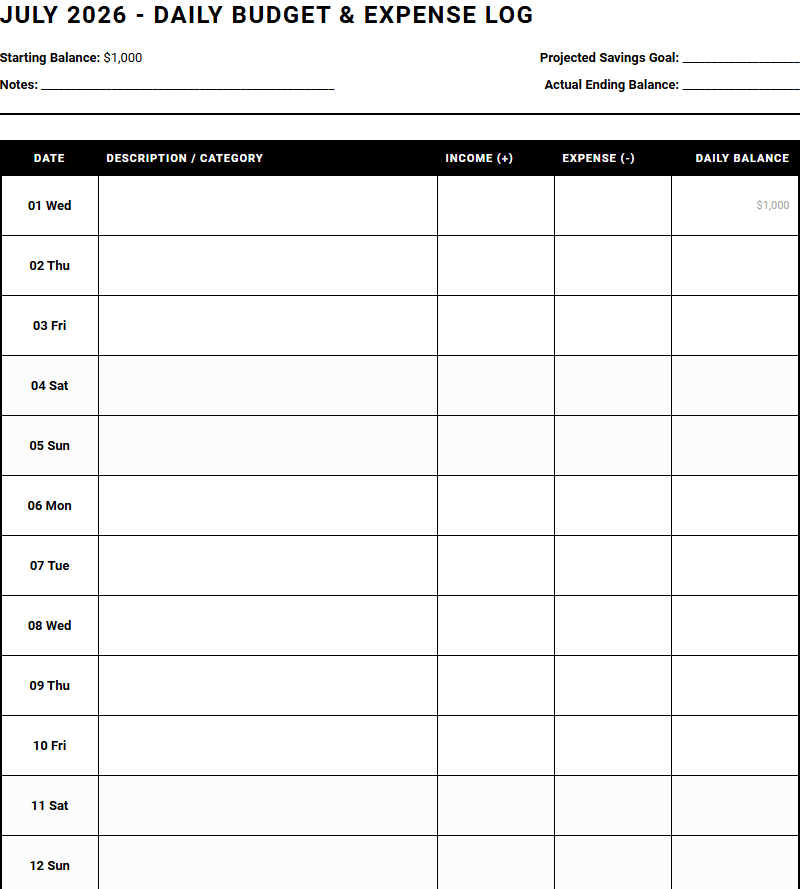

Managing daily cash flow and tracking micro-expenses often feels overwhelming, leading to unexpected budget deficits. While stable income streams and traditional monthly spreadsheets offer a broad financial overview, the Daily Agendas printable calendar grants immediate, granular visibility over your spending.

Though this system requires consistent daily logging to be effective, tracking small, routine purchases like transit fares or coffee runs quickly reveals hidden leaks. Below, we outline how to utilize this printable tool to master your Budget and Expense Daily Log.

Create Your Budget And Expense Daily Log

Done customizing?

Budget And Expense Daily Log - Good to Know

Zero-Based Budgeting

Zero-based budgeting is a highly structured financial strategy where your total income minus your total expenses equals exactly zero. Unlike traditional budgeting methods that carry over spending habits from previous months, this approach requires you to justify and allocate every single dollar you earn to a specific category. This includes necessities, savings, debt repayment, and investments.

By giving every dollar a specific job, you eliminate passive spending and force yourself to become actively aware of where your money goes. This meticulous planning is ideal for individuals looking to maximize their savings potential or accelerate their debt payoff journey.

- Income Allocation: Assigning every cent of your monthly paycheck to a designated category.

- Active Oversight: Restructuring your categories monthly to reflect fluctuating seasonal expenses.

- Financial Discipline: Preventing impulse purchases by ensuring no unallocated funds remain.

Cash Stuffing

Cash stuffing is a tactile, visual financial management system that has experienced a massive resurgence among modern savers. Under this system, you withdraw your discretionary income in physical cash at the beginning of each pay period. You then distribute these paper bills into physical, labeled envelopes designated for specific spending categories, such as groceries, dining out, entertainment, and beauty services.

Once an envelope is empty, you cannot spend any more money in that category until the next month begins. This physical barrier prevents the effortless overspending associated with tap-to-pay cards and digital wallets.

- Withdraw your predetermined discretionary funds from the bank.

- Distribute the physical bills into designated envelopes or binder sleeves.

- Spend exclusively from these envelopes, leaving debit and credit cards at home.

Kakeibo

Kakeibo, which translates to "household account book," is a traditional Japanese budgeting method that emphasizes mindfulness and deliberate reflection over cold, clinical mathematics. Introduced in the early twentieth century, this paper-and-pen method asks users to answer four key questions regarding their finances: How much money do you have available? How much would you like to save? How much are you actually spending? And how can you improve?

Rather than relying on automated apps, Kakeibo encourages you to manually write down every purchase and categorize it into four distinct areas: Survival (needs), Optional (wants), Culture (books, museums), and Extra (unexpected costs).

"Kakeibo shifts your financial mindset from one of deprivation to one of mindful awareness, helping you understand the emotional triggers behind your spending."

Sinking Funds

Sinking funds are targeted savings accounts designated for specific, non-monthly expenses that you know are coming down the pipeline. Unlike a general emergency fund, which is reserved for unexpected catastrophes like sudden medical bills, sinking funds are designed for predictable, planned expenditures. Examples include annual car insurance premiums, holiday gifts, home maintenance, or a planned vacation next summer.

By dividing the total expected cost of these items by the number of months remaining before the payment is due, you can save incrementally without disrupting your monthly budget.

- Stress Reduction: Eliminates the panic of large, predictable annual bills.

- Precision Saving: Keeps your primary savings untouched and protected.

- Intentional Planning: Allows you to enjoy big purchases completely guilt-free.

Micro-Expense Tracking

Micro-expense tracking focuses on logging the smallest financial transactions that routinely slip through the cracks of broader budget categories. While most people remember to track their rent, car payments, and utility bills, they often overlook the impact of small, daily habits. The three-dollar coffee, the parking meter fee, or the occasional digital media rental can quietly drain hundreds of dollars from your bank account each month.

By logging every single transaction, regardless of how trivial the amount seems, you gain a realistic view of your true financial habits. This granular tracking often reveals surprising patterns, allowing you to make small adjustments that yield significant long-term savings.

Paying close attention to these minor transactions creates a stronger overall financial foundation by eliminating hidden leaks in your cash flow.

Subscription Audit

With the rise of the modern subscription economy, many consumers are paying for services they rarely or never use. A subscription audit is a systematic review of all recurring payments, including streaming platforms, software licenses, gym memberships, and meal delivery kits. Many of these services operate on auto-renewal models, quietly charging your accounts without sending prominent receipts or notifications.

Conducting an audit requires you to print your bank and credit card statements from the past three months, highlight every recurring charge, and ruthlessly evaluate its utility.

- Identify all active subscriptions across all payment methods.

- Evaluate the usage frequency and cost-to-value ratio of each service.

- Cancel underutilized memberships immediately to reclaim passive losses.

Discretionary Spending Log

A discretionary spending log is an active journal dedicated solely to recording non-essential purchases. While fixed expenses like rent and insurance are non-negotiable, your discretionary spending is highly variable and entirely within your control. This log tracks everything from clothing and home decor to dining at restaurants and recreational activities.

By separating these variable expenses from your fixed costs, you can easily identify where your flexible income is being directed. Reviewing this log weekly allows you to adjust your behavior in real-time before you overspend, rather than realizing your mistakes at the end of the month when it is too late to make corrections.

- Track clothing, entertainment, hobbies, and dining experiences.

- Monitor daily impulsive spending habits in real-time.

- Adjust variable spending dynamically to meet your monthly financial targets.

No-Spend Days

A no-spend day is a self-imposed financial challenge where you commit to spending absolutely zero dollars for a full twenty-four-hour period. This means no grocery trips, no online shopping, no buying coffee on the way to work, and no ordering takeout. The only exceptions are pre-existing, automated bills like rent or utilities.

Implementing no-spend days helps break the cycle of casual, impulsive spending and forces you to find creative ways to use resources you already possess, such as cooking meals with ingredients already in your pantry or finding free local entertainment. This practice resets your relationship with money, highlighting how often we spend out of boredom rather than genuine necessity.

Regularly scheduling these days builds financial resilience and accelerates your progress toward saving goals.

Envelope Method

The envelope method is the foundational framework behind modern cash-based budgeting. This classic technique involves dividing your disposable income into various physical envelopes labeled with specific expense categories at the beginning of each pay period. When you go shopping, you only use the money contained in the corresponding envelope.

This system relies on the psychological pain of parting with physical cash, which is proven to reduce spending compared to swiping a plastic card. It prevents overspending by establishing a hard, physical limit on your resources. When the envelope is empty, your spending in that category must cease completely until the next cycle.

- Creates an immediate physical boundary for discretionary purchases.

- Saves money by removing the temptation of digital credit lines.

- Builds a deep, intuitive understanding of your immediate purchasing power.

Cash Flow Ledger

A cash flow ledger is a comprehensive tool used to track the exact timing of both your income and your expenses. Unlike standard monthly budgets that assume all income and expenses happen simultaneously, a cash flow ledger maps out transactions chronologically. This is particularly valuable for individuals with irregular income streams, freelancers, or those who find themselves struggling with cash flow mismatches between paydays.

By visualizing exactly when money enters your account and when bills are due, you can plan your payments strategically, avoid overdraft fees, and ensure you always have a comfortable financial cushion to cover upcoming liabilities.

"A cash flow ledger bridges the gap between earning and spending, ensuring your funds are available exactly when they are required."

Leave a comment