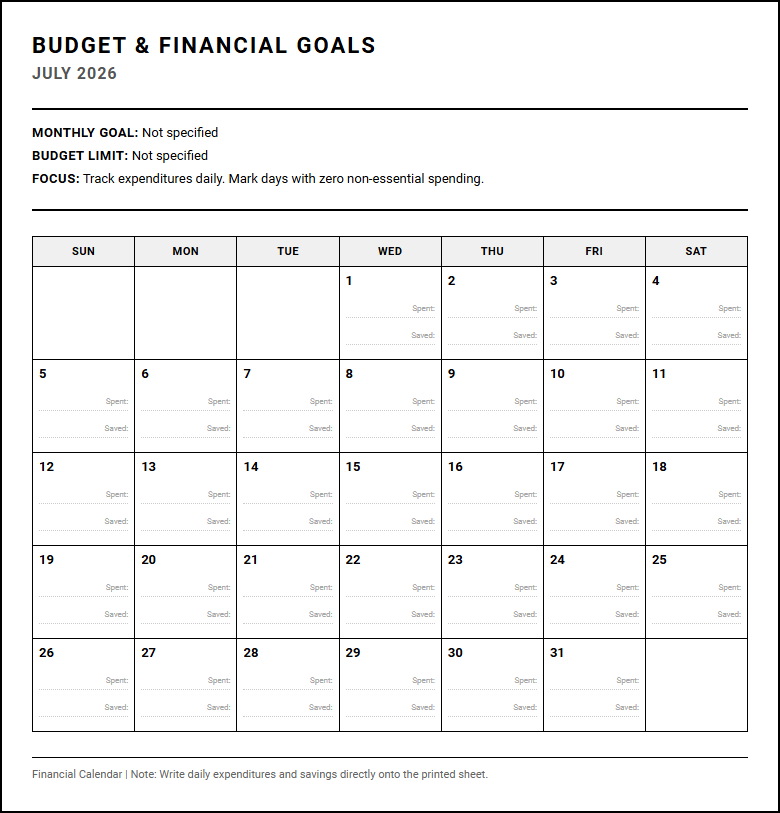

Staying on top of personal financial milestones can feel overwhelming. While digital banking apps and complex spreadsheets offer raw transaction data, they often lack a tangible connection to your daily routine.

A dedicated printable Budget and Financial Goal Calendar grants you immediate visual clarity and control. However, this tool is most effective when paired with a consistent weekly review habit. By visually plotting concrete targets-such as a $500 emergency fund milestone-you build steady momentum.

Below, we explore how to leverage this printable calendar to transform abstract financial targets into actionable daily habits.

Create Your Budget and Financial Goal Calendar

Done customizing?

Budget and Financial Goal Calendar - Good to Know

Cash Flow Calendar

A Cash Flow Calendar is an essential visual tool designed to map out your exact financial inflows and outflows over a specific month. Unlike traditional monthly budgets, this calendar focuses on the precise timing of your money. By plotting your paydays alongside scheduled bill due dates, you can easily identify potential liquidity gaps before they occur.

To implement this system effectively, consider tracking the following key elements:

- Income Deposits: Mark exact dates for primary paychecks, side hustle earnings, or investment dividends.

- Fixed Expenses: Note recurring payments such as rent, mortgages, insurance premiums, and utility bills.

- Discretionary Spending Windows: Highlight periods where cash reserves are high, allowing for safer non-essential purchases.

Using this structured temporal approach prevents the common frustration of being temporarily short of cash, even when your total monthly income technically covers your overall monthly expenses.

Sinking Funds Tracker

The Sinking Funds Tracker is a proactive financial strategy designed to handle large, non-annual expenses without disrupting your daily budget. Instead of facing sudden financial shocks from seasonal events, you systematically save small amounts over time. This approach transforms overwhelming future bills into manageable, bite-sized monthly contributions.

Common categories managed through this tracker include:

- Annual vehicle registration and insurance premiums

- Holiday shopping and birthday gifts

- Home maintenance and emergency appliance replacement

- Planned medical co-pays or veterinary visits

By maintaining a dedicated spreadsheet or utilizing separate digital sub-accounts, you can monitor your progress toward each specific goal. This targeted savings method ensures that when these inevitable expenses finally arrive, the cash is already waiting, protecting your long-term investment accounts from untimely liquidations.

Zero-Based Budgeting

Zero-Based Budgeting (ZBB) is a highly disciplined financial framework where every single dollar of your monthly income is allocated to a specific purpose. The core mathematical principle of this method is straightforward: Income minus Expenses equals Zero. This does not imply that your bank account hits zero, but rather that every dollar is intentionally directed toward savings, debt payoff, or living expenses.

By forcing yourself to justify and assign a job to every unit of currency, you eliminate mindless spending habits. Users of this methodology typically categorize their funds into:

- Active Spending: Groceries, fuel, and utilities.

- Future Allocation: Retirement contributions and emergency fund growth.

- Debt Reduction: Extra payments toward credit cards or student loans.

This deliberate prioritization ensures maximum financial efficiency, turning passive earners into highly conscious asset allocators.

Cash Stuffing

Cash Stuffing, traditionally known as the envelope system, is a tangible budgeting methodology that leverages physical currency to curb impulsive spending. By withdrawing your discretionary income in cash and distributing it into labeled envelopes, you establish hard, physical boundaries for different spending categories.

This tactile system offers several psychological and practical advantages:

- Immediate Visual Feedback: You can instantly see exactly how much money remains in your dining out or entertainment budget.

- Friction-Based Spending: Handing over physical bills creates psychological pain, naturally reducing unnecessary purchases.

- Strict Spending Caps: Once an envelope is empty, spending in that category must cease until the next budgeting cycle.

For modern consumers, this practice can also be replicated digitally using virtual banking envelopes or sub-accounts. It remains an excellent entry-point strategy for individuals looking to break the cycle of subconscious digital overspending.

Financial Milestone Mapping

Financial Milestone Mapping is the strategic practice of plotting your long-term economic objectives onto a chronological timeline. By translating vague aspirations into concrete, time-bound milestones, you create a structured roadmap for your financial lifetime. This method bridges the gap between daily budgeting and decades-long wealth accumulation.

An effective milestone map categorizes goals into distinct temporal horizons:

- Short-Term Milestones (1–2 Years): Building a six-month emergency reserve or paying off high-interest personal loans.

- Medium-Term Milestones (3–7 Years): Securing a down payment for real estate or funding advanced educational degrees.

- Long-Term Milestones (10+ Years): Achieving complete financial independence or establishing generational wealth trusts.

Consistently updating this map ensures that your daily spending choices remain aligned with your deepest, most significant life ambitions.

Payday Budgeting

Payday Budgeting is an agile financial management system structured entirely around the frequency of your compensation cycles. Rather than managing your money on a rigid calendar-month basis, you create a mini-budget each time a new paycheck is deposited. This method is highly effective for individuals with bi-weekly, weekly, or irregular income streams.

When implementing this system, each paycheck is immediately divided into three core functional pillars:

- Immediate Obligations: Bills and expenses due before the next payday.

- Future Security: Automatic transfers to savings accounts and retirement portfolios.

- Lifestyle Allocation: Variable spending money to last until the next cycle.

This dynamic approach prevents the stress of the end-of-month cash squeeze, ensuring that your immediate living costs are always covered in real-time as your income arrives.

Money Minute Routine

The Money Minute Routine is a highly efficient, daily financial check-in that takes sixty seconds or less. By committing to a brief daily review of your accounts, you demystify your personal finances and eliminate the anxiety associated with opening your banking applications. This habit transforms financial management from a dreaded monthly chore into a seamless daily ritual.

During this sixty-second routine, you focus on three rapid verification points:

- Transaction Verification: Quickly scan yesterday's transactions to identify any unauthorized charges or banking errors.

- Balance Awareness: Note your current checking account balance to guide your spending decisions for the day.

- Goal Alignment: Briefly remind yourself of your active savings goals to keep impulse spending in check.

This consistent, low-friction practice builds immense financial confidence and helps catch fraud or budgetary deviations instantly.

Debt Snowball Schedule

The Debt Snowball Schedule is a highly acclaimed debt-elimination strategy popularized by personal finance experts. This methodology prioritizes psychological quick wins over strict mathematical interest rates. You list your liabilities in order of total balance size, from the absolute smallest to the largest, regardless of the corresponding interest charges.

The operational execution of this schedule follows a structured sequence:

- Maintain minimum payments on all outstanding debts except the smallest one.

- Direct all extra budget surpluses and windfalls toward paying off the smallest debt.

- Once the smallest debt is eliminated, roll its entire monthly payment amount into the next smallest balance.

This compounding payment momentum creates a powerful psychological "snowball" effect, building your motivation and confidence as liabilities disappear one by one from your balance sheet.

Automated Savings Calendar

An Automated Savings Calendar is a hands-off financial system that utilizes technology to build wealth effortlessly. By coordinating automatic bank transfers with your income cycles, you remove human emotion, willpower, and procrastination from the savings equation. This strategy ensures that you pay yourself first before any discretionary spending can occur.

To optimize your automation schedule, align your transfers with these specific financial events:

- Payday Sweeps: Automatically move a fixed percentage of income directly into a high-yield savings account on payday.

- Mid-Month Adjustments: Route smaller, automated micro-transfers to specialized sinking funds.

- Investment Contributions: Schedule recurring drafts to brokerage accounts or retirement portfolios to leverage dollar-cost averaging.

Automating these processes ensures consistent, disciplined progress toward your financial goals without requiring active, daily decision-making.

Net Worth Tracker

A Net Worth Tracker is the ultimate metric for measuring your overall financial health and long-term progress. Your net worth is a simple but powerful calculation: Total Assets minus Total Liabilities. By updating this metric regularly, you shift your focus away from mere income levels and toward genuine, long-term wealth accumulation.

To maintain an accurate tracker, you must systematically update both sides of your personal balance sheet:

- Assets (What You Own): Cash reserves, retirement accounts, investment portfolios, real estate equity, and valuable physical property.

- Liabilities (What You Owe): Mortgages, car loans, student loans, credit card debt, and personal lines of credit.

Tracking this figure quarterly or annually provides an undeniable visual representation of your financial trajectory, keeping you motivated to increase your investments while aggressively reducing outstanding consumer liabilities.

Leave a comment